Blog

The ECDB Blog turns data from the Tool into eCommerce insights that illustrate which use you can make of our comprehensive data. It elaborates on relevant eCommerce news to help your brand gain a broader perspective on current retail trends and their effects. Our articles are carefully crafted to present to you the latest market trends, including retail, payment, shipping, transactions, cross-border and more.

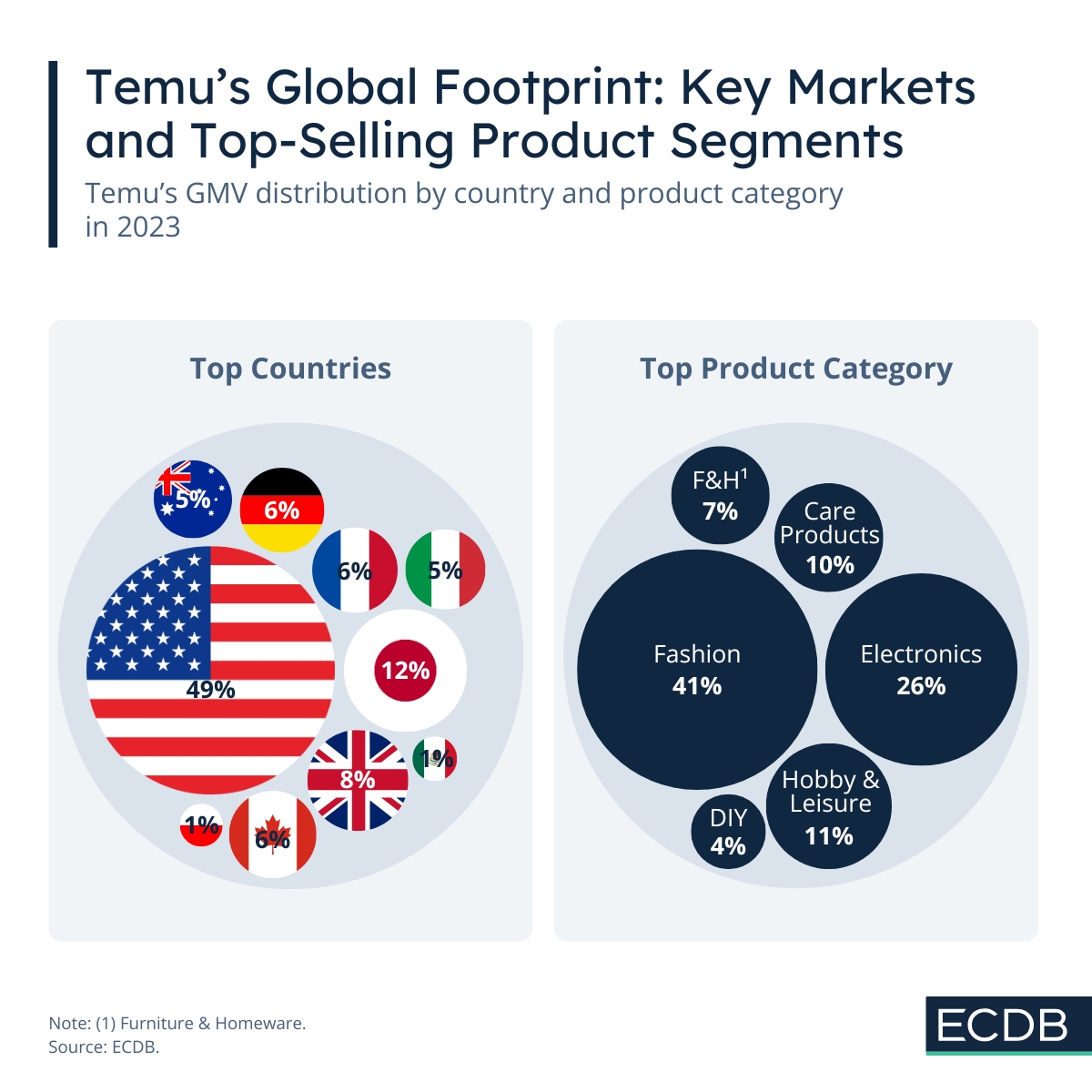

Temu in the West: Just Hype or the Future of eCommerce?

Temu, the budget-friendly online marketplace owned by PDD Holdings, has exploded in popularity with its F2C business model. The U.S. and European markets are key regions.

Item 1 of 5

All Articles

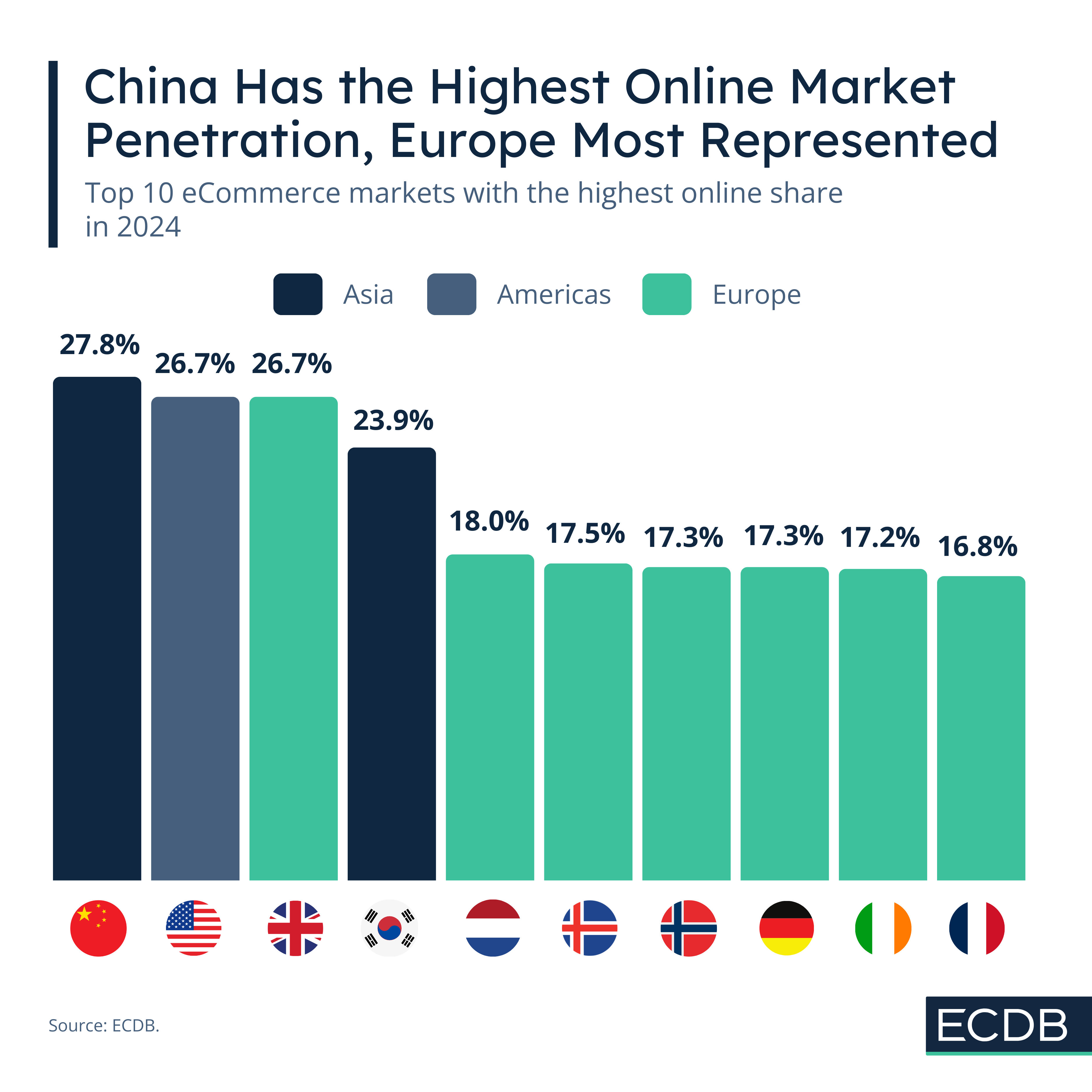

China Has the Highest eCommerce Penetration in the World

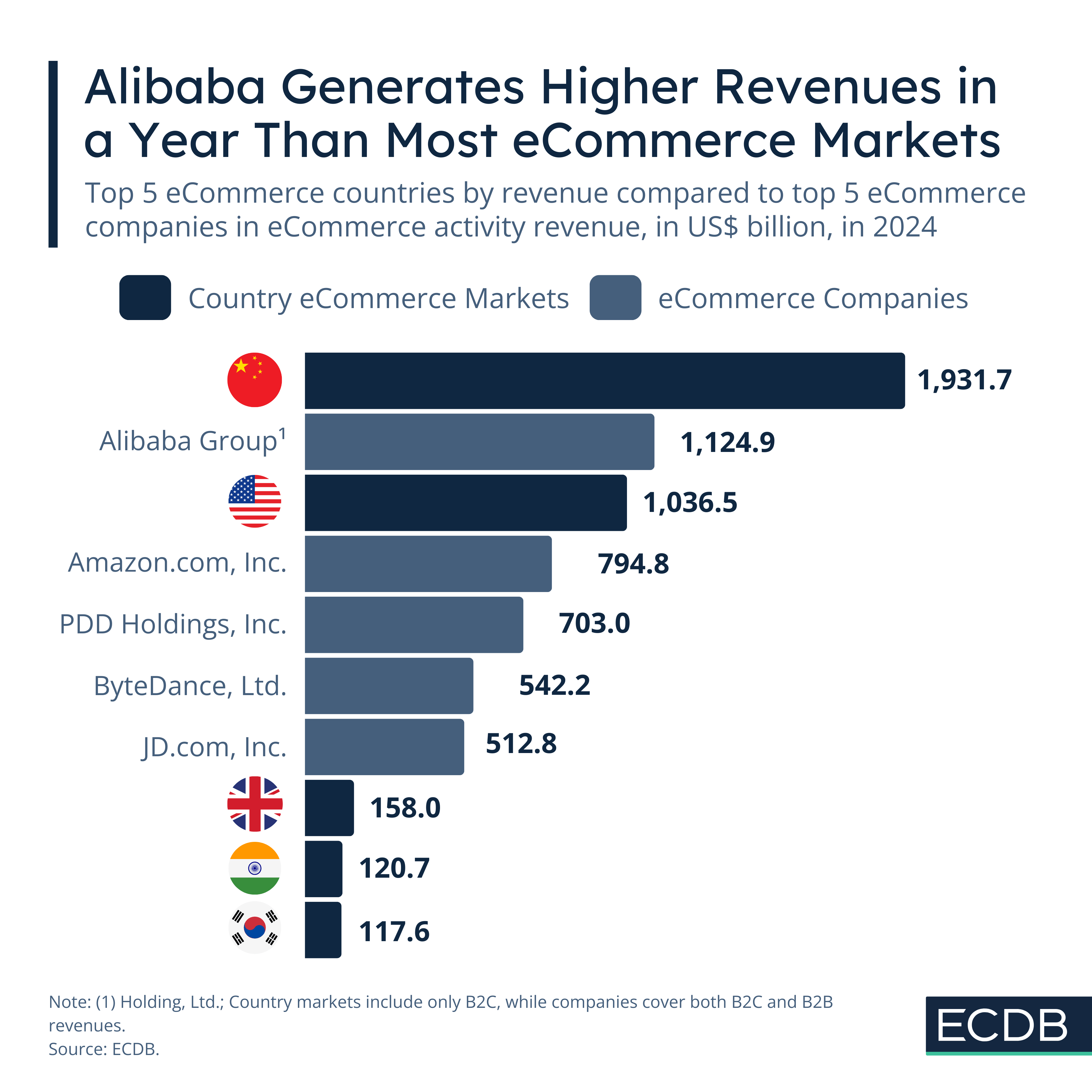

The Top 5 eCommerce Companies Generate Higher Revenues Than Most Countries

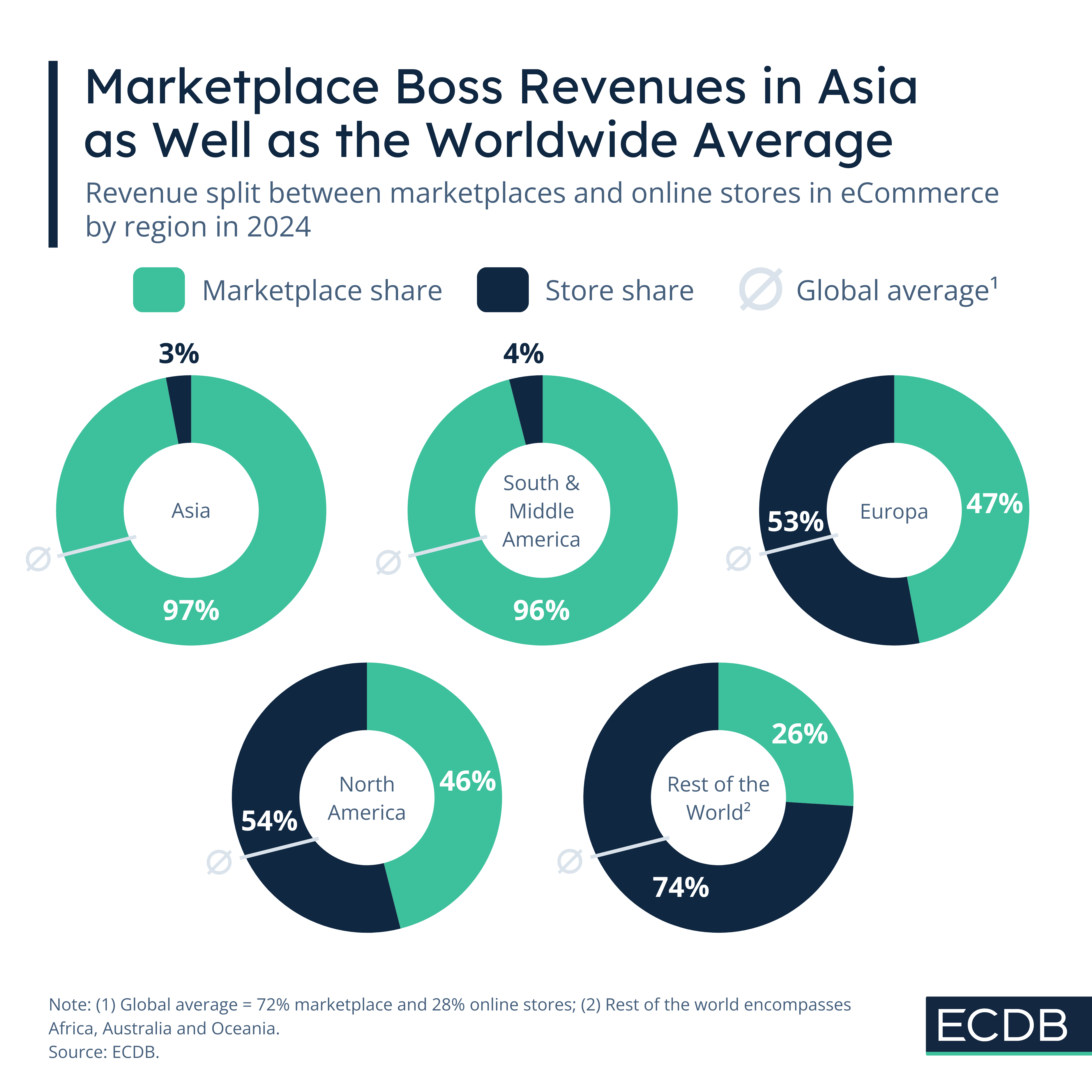

Marketplace vs. Online Store – Which Business Makes the Race?

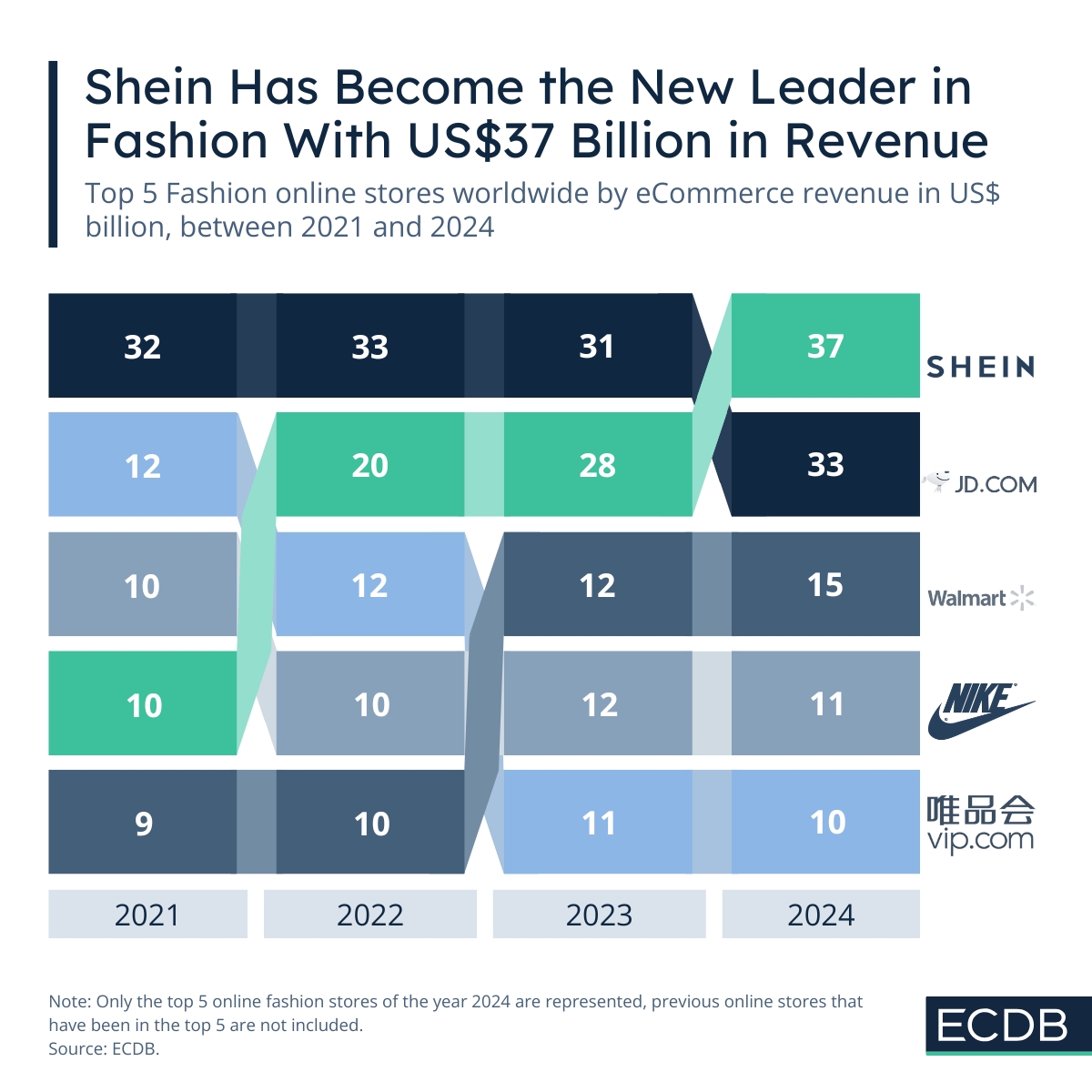

The Fashion eCommerce Market Has a New Leader: Shein Climbs to the Top

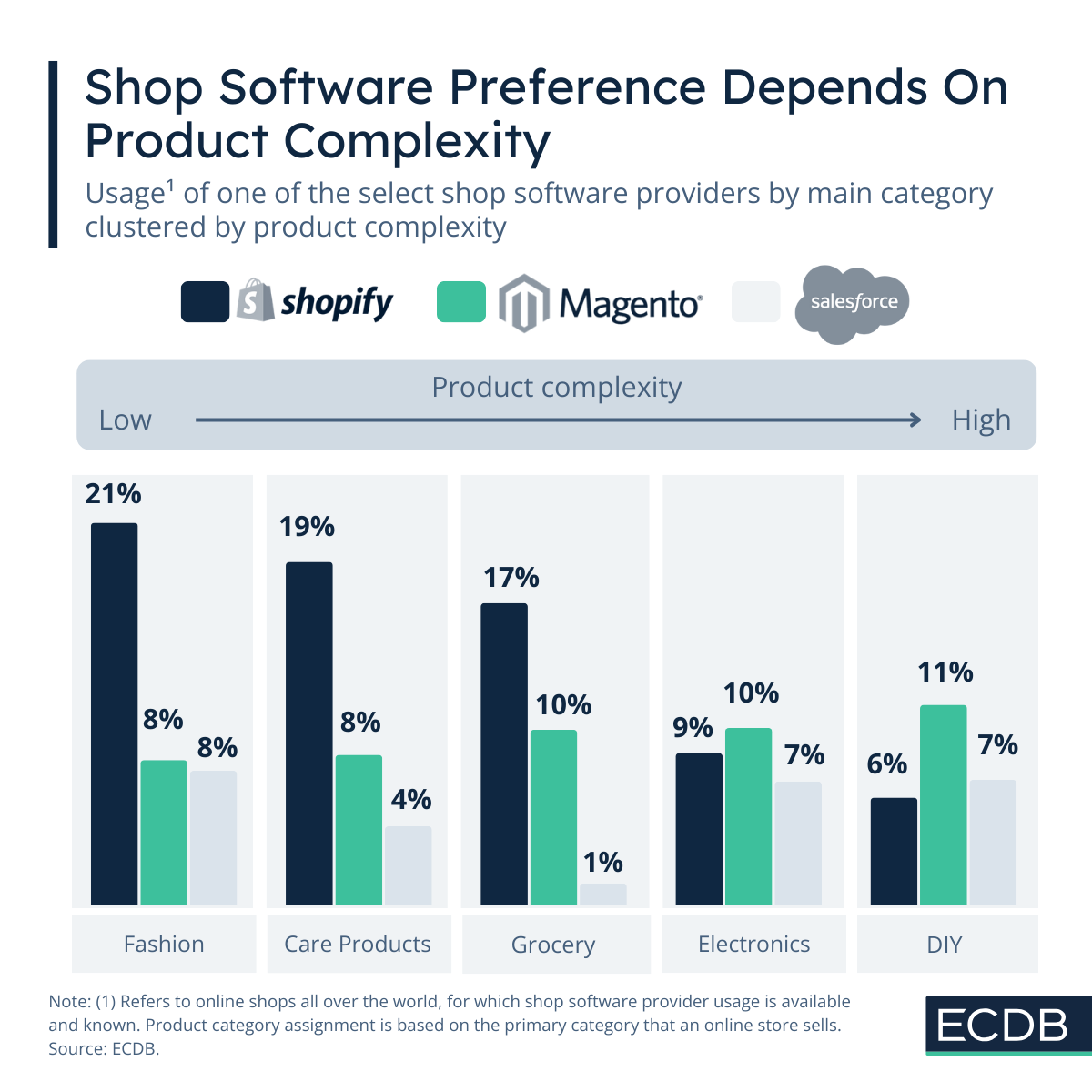

Here Is How Product Categories Shape the Choice of Shop Software

Ready To Get Started?

Find your perfect solution and let ECDB empower your eCommerce success.